Was Girl Math Invented By A Man?

Was Girl Math Invented By A Man?

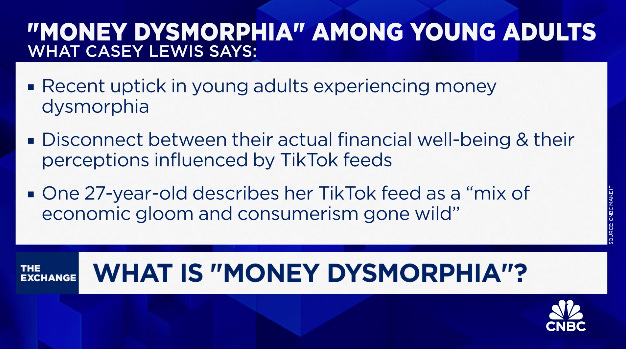

Coping with money dysmorphia + girl math

Last week, I explored the Croissant app and realized they’re not really offering discounts or savings on clothes—they’re selling a false sense of psychological security with their buyback option. It may look and feel like a deal, but it’s worth considering if it’s more of an illusion than a guarantee.

This isn’t surprising; most brands today focus on selling ideas more than products. If I learned anything from my experience in marketing, it’s that people aren’t really buying things anymore—they’re buying what those things represent.

At first glance, Croissant seemed like a financial win, but when you break it down, it’s more of a gamble than a sure thing. The terms are limited, and the resale conditions can be tough to meet. Compared to renting, owning, or buying used, banking on reselling new retail clothing isn’t a smart move—it’s a bet your mind perceives as a win before the win actually happens.

This false sense of security feels perfectly timed, especially when you consider the current attitudes of Gen Z and Millennials toward money.

According to ThredUp’s Resale Report, 82% of Gen Z shoppers prioritize buyback value when making purchases. Meanwhile, 2 in 5 Americans have used “buy now, pay later” schemes, often leading to overspending and missed payments. 1 in 7 Gen Z credit card users are maxed out, carrying more debt than any other generation at the same age.

All of this led me to discover money dysmorphia, a condition affecting young adults where they have a distorted perception of their finances. It can result in irrational behaviors like overspending, extreme frugality, or constant financial anxiety—regardless of their actual wealth.

My first reaction was total identification. In my 20s, I racked up significant credit card debt. I didn’t grow up with money, but I ended up surrounded by wealthy classmates in school and later worked with people from similar backgrounds. I couldn’t shake the feeling that the universe had mixed up my paperwork and put me in the wrong tax bracket at birth. My soul was very rich, I deserved nice things, and I figured, why not start living that way now?

What I didn’t realize was that a $17 plate of calamari could cost $90 after years of credit card interest. I learned the hard way, facing fees and the worst credit woes when I had the least money to deal with them.

I tightened up and lived like a monk for a while—even renting out my apartment on Airbnb occasionally to crash with friends. I was underpaid, broke, and constantly chasing extra cash. Looking back now, I wonder: is “financial dysmorphia” just a fancy term for being poor?

But then I remembered how I felt when, years later, I finally achieved real financial security. I was in shock. I’d hit my financial goals and feel nothing. I’d immediately set new ones. The ceiling kept rising, and the money was both thrilling and terrifying. The more I made, the worse I felt. I never truly felt safe. When I mentioned this to my therapist at the time, she suggested I might have “sudden wealth syndrome”—a condition where going from broke to wealthy causes isolation, guilt, and uncertainty—essentially, an identity crisis.

Now, I’m no longer at either extreme—crushed by overdraft fees or cushioned by a high-paying job that came at the expense of others. And honestly, while diagnoses like “money dysmorphia” or “sudden wealth syndrome” make some sense, they also make me laugh a bit now.

Sure, people are unwell, but labeling them with diagnoses often sidesteps the real issue. It’s easier to call normal reactions to harsh conditions and a consumption driven society pathological than to admit the system itself is broken and unsustainable.

Whether I was broke or wealthy, something always felt off. The fact that my situation could flip so quickly—from struggling to suddenly secure—without anything fundamental in me changing, was unsettling. It made the world feel unfair and irrational. The idea that hard work alone leads to wealth is harmful, because it’s simply not true. Financial security often involves a mix of hard work, privilege, luck, and, too often, the exploitation of others.

I felt displaced both when I wasn’t making money and when I was. It all felt fragile—like something I faced alone, whether I was struggling or doing well. Without money, I felt isolated and ashamed, like I was failing. And with more money, I still felt isolated, knowing financial security wasn’t accessible to most people, even those closest to me.

It was hard to have an honest conversation about this with anyone. People rarely talk about money honestly—we’re oddly secretive about it, even though we live in a society where people constantly overshare about everything else, including their irritable bowel syndrome…

We get subtle hints—“I went on vacation to Italy” or “I got a promotion and doubled my income.” But money remains a black box that’s hard to decipher. Did that trip put you in debt? Were you severely underpaid before the promotion?

Then there are the anecdotes: “Do what I did, and it’ll work for you too!”—even if my life comes with advantages yours doesn’t, making it unlikely to work the same way for you.

We’re drawn to tips and tricks—“hacks” for spending. Take “Girl Math,” for example, which started as a joke—a playful way to justify financial habits.

Returned an expensive dress? “Girl math” might tell you that you’ve made money, even though you’re just getting back what you spent. It’s about justifying purchases by squeezing the most out of money that’s already gone, similar to the accounting concept of sunk costs. It’s a way to make spending feel okay, but it highlights how we convince ourselves something is worth it, even when the money is already gone and can’t be recovered.

I don’t think most people actually take “girl math” seriously. It’s a joke that highlights the funny ways we justify irrational spending—like spending $75 more just to avoid a $5.99 shipping fee. Lately, I’ve noticed “girl math” creeping into sales pitches, and I wonder if people are starting to take it as real financial advice. I’ve also seen nonsensical cost-per-wear calculations being used to justify outrageously expensive purchases.

Last winter, I took a look at the High Sport pants after seeing people justify their $860 pant purchase. Someone claimed they’d already gotten the cost down to a dollar per wear. But here’s the catch: the ones doing the math were selling the pants.

The numbers didn’t add up. To get the cost down to a dollar per wear, you’d need to wear them over 900 times. Considering they’ve only been available for a couple of years, unless the calendar suddenly has 700 days or you’ve been surgically attached to them for 2.5 years straight, that math just doesn’t check out.

It feels less fun and more unfair when women are encouraged to dismiss basic math and embrace ideas like “girl math” or “cost per wear” without much thought. While these concepts can be playful, they don’t always reflect reality and might lead to overlooking smarter financial decisions. For example, an ad for Croissant even claimed, “At least it’ll help us sharpen our math skills!”

Spoiler: it probably won’t.

Has “girl math” shifted from a joke to a coping mechanism, a marketing pitch, or both? It’s a way to laugh off spending instead of admitting the marketing worked. But pretending we didn’t know better doesn’t really help? Sometimes, we just make bad decisions—and that’s okay. The more I can say, “Well, that didn’t go as planned, and that sucks,” the more I learn and avoid repeating it. But facing that truth is tough, so instead, we convince ourselves, “I got them—they didn’t get me!”

Women make 85% of consumer purchases in the U.S. but represent only 13% of CEOs. Some argue it’s misogynistic to judge how women spend their money, but the real issue is treating women as cash cows. Misogyny thrives when women are encouraged to spend and fuel the economy but are denied real financial control or opportunities to build net worth.

The story that spending equals empowerment works well for those who profit from you buying more. Women are prime targets for this kind of “empowerment” narrative. But real empowerment isn’t just about spending—it’s about gaining the opportunities and control needed to build lasting financial security.

In response to all of this, I’ve developed my own strange coping mechanisms. Here are a few of them.

(Opportunity) Cost Per Wear

“Cost per wear” justifies a purchase by lowering the cost each time you wear it, making it feel like more value over time. But lately, I’ve been thinking about something I call “Opportunity Cost Per Wear”—the trade-off between your money and your life.

Every dollar spent isn’t just about buying something—it’s the time, effort, and energy you invested to earn that money. Are you swapping your well being and future security for something that’s only going to make you happy right now? Sometimes spending on certain things can end up keeping you tied down longer, adding extra stress, and delaying the freedom we all want.

A couple examples:

When you’re considering high-ticket items like a $1,300 bag, it’s worth thinking beyond the immediate cost. If you invested that $1,300 in a ROTH IRA with a 10% annual return, in five years it could grow to around $2,095—$795 more than if you spent it. I need to create an app that shows my bank account balance and net worth in the corner of my browser instead of a coupon plugin. It could flash reminders like, “Girl, the stock market is crashing, and your 401k is down,” or “Take a breath, this purchase is adding two more months of work to your life.”

If you put a $1,300 bag on a credit card with a 25% APR and make only minimum payments over 5 years, you’d end up paying around $1,600—making that bag more expensive than you imagined. Consumer debt felt like a constant weight, draining my energy and making me feel like I was always running just to stand still. I’d rather give up instant gratification for the real win—relaxing and finding happiness in the freedom of being debt free.

So, while “cost per wear” could justify a purchase, “opportunity cost per wear” also tells a different story. When you factor in missed rent payments, fees, interest, credit damage, extra work years, missed investment opportunities, and donations to those in need, that item could end up costing much more than you realized. The trade-off between immediate gratification and long term financial gain becomes clearer when you consider all the hidden costs.

Just Look at Photos Of Older White Men

Last week, I researched Croissant’s billionaire investors and—no surprise—they were mostly wealthy white men. I imagined them at a villa, overlooking the ocean, raising a glass and saying, “Women be shopping!” It hit me: I don’t need to make any more rich white men richer. This visual will save me more than any shopping plugin ever will.

I went looking at fall sweaters and checked out Jenni Kayne. The sweater price? $595. The sole investor? Her billionaire father, Richard Kayne.

It was fun to Google his name and find one of the top results was SUPER YACHT DOT COM. I took a YouTube tour of Ric’s $45 million superyacht, Suri, while polishing off a $4.50 cookie bucket from Costco. I realized, why settle for a sweater when I could help the fam out and rent their yacht for just $350,000 a week instead?

Do all roads lead to an old white guy? I went digging for one behind the private equity firm that owns Reformation, and bingo! Found the founder of Permira Equity Group—classic. But plot twist: he exited a while ago. Now he’s too busy doing philanthropy to take the blame. What a letdown.

But fear not, the previous old white man has moved on—only to be replaced by a future one in training. Meet the current head of Permira Equity, majority owner of Reformation… still keeping the tradition alive!

Let’s be real: not every old white guy is evil. Some of the people I love most fit that description! But when I scroll through these photos, I’m just reminded of who holds the majority of wealth: white men. Whatever the reason, this visual is helping me cope. So if you can have your “girl math,” please, just let me keep my old white dudes.

There Is No Safety Net (And That’s Basically The Human Experience)

My weirdest but most effective coping mechanism for financial dysmorphia? Accepting that there’s no real security. Money comes and goes, and no amount of planning, investing, or buying nice things can shield me from life’s inevitable challenges.

Resisting this reality only makes things harder. This “crazy” mindset of “financial dysmorphia”—comes from the lack of a real safety net in America. A recent headline summed it up perfectly: “America Doesn’t Have a Safety Net; It Has Women.”

I don’t have to tell you there’s no future-proofing here. Get sick, and your savings vanish. There's no guaranteed parental leave, paid time off and very little communal care to rely on. Gen Z’s debt isn’t just from reckless spending—it’s a survival tactic in an increasingly tough world. Financial struggles reflect larger systemic issues, not just a shopping addiction. When things go wrong, you’re often on your own. We’ve built a society that pushes individualism and consumerism as coping mechanisms instead of real, systemic support. No wonder we turn to spending to fill the gaps.

When I say I’ve accepted that there’s no safety net, I don’t mean that I’m doom spending and going on a buying spree, calling it “self-care” as the world falls apart. I still want to make the world a better place, but that often means stepping offline, engaging with my local community, and working toward better alternatives—even if I won’t see them in my lifetime.

The best thing I’ve ever done for my wallet? Accepting that life is uncertain. We live in a world that pushes us to consume and chase happiness, so when normal suffering hits, it feels wrong—even though it’s natural. Life will break your heart. We’ll all witness suffering and loss. Instead of avoiding it, I try to lean into it, which somehow makes life feel more vivid.

When I realize that life is fragile for everyone, it doesn’t make me panic—it makes me appreciate it more. Why keep hoarding clothes for “someday” while constantly adding more? Isn’t that just ignoring the present? How can I show up today and hold the hand of someone I love before it’s too late and I realize I took them for granted?

So many stories we were told about a safety net

But when I look for it, it's just a hand that's holding mine —Caroline Polachek

I don’t buy much anymore. I still love clothes, but I’ve realized that most of the time, I’m just buying into a fantasy (which can be fun—and kind of the point!). Now, I’m more mindful when I indulge in that fantasy—though sometimes I still do, because I’m human, and I make space for that too. Recently, I bought some amazing heels for a wedding, and this time, it wasn’t just about chasing a high—it was a purchase I plan to enjoy for years.

I’m also learning to be okay with having less than what society says I need (though less still feels like a LOT!). We’re constantly encouraged to chase fleeting dopamine hits or get frustrated when we don’t get what we want right away. But living like this is its own kind of hell. The quality of our lives is rooted in the quality of our minds, and I’m working on finding the balance between being content with what I have while still allowing myself to want more—not just for me, but for everyone.

What are you experiences with financial distortion? Do you feel pressure to shop like a millionaire, even before securing your financial future? Do you ever feel pressured to justify your purchases with ideas like “girl math” or “treat yourself” culture?

🍒Total Rec

Have a topic you’d like to me to explore, a product you want to review, or something you want to share with me anonymously? Put it on my Total Rec Radar here.

If you appreciate the time and effort that has gone into this newsletter, consider upgrading to paid or making a donation here:

The white man sweater mashups are REALLY going to help me. You’re brilliant and hilarious my girl, keep it up

I’ve been waiting for this essay! Please turn this into a book about marketing, gender, behavior patterns, and money. And look at how to first change perception, and then habits. It would be a best seller.

I’d buy it without doing any math. 💗